A home equity loan is money you can borrow by using your house as security. Think of it like a loan that lets you tap into the value your home has built over time. If your house is worth more than what you owe on it, you have equity. The bank can lend you money based on that equity. It’s like borrowing from your house to pay for things like home repairs, school, or even a vacation!

People love home equity loans because they usually have lower interest rates than other loans. But it’s important to understand how it works so you don’t get into trouble. This guide will help you learn everything about home equity loans with easy words and clear examples.

How Does a Home Equity Loan Work?

When you get a home equity loan, you borrow a lump sum of money all at once. You then pay it back over time with a fixed interest rate. This means your monthly payments stay the same, which makes budgeting easier.

Banks look at your home’s value and subtract what you still owe on your mortgage. The leftover amount is your equity. Usually, lenders let you borrow up to 80-85% of your home’s equity. For example, if your home is worth $300,000 and you owe $200,000, you have $100,000 in equity. The bank might let you borrow up to $80,000 of that.

Benefits of a Home Equity Loan

Home equity loans can be great because:

- Lower interest rates than credit cards or personal loans.

- Fixed monthly payments, so you know what to expect.

- You can borrow a big amount at once.

- Interest might be tax-deductible (check with a tax expert!).

People often use these loans for home upgrades, debt consolidation, or big expenses like college tuition.

Risks of Using a Home Equity Loan

Though helpful, there are risks:

- Your home is the loan’s security. If you don’t pay back, the bank can take your home.

- You might borrow too much and get into debt.

- Fees and closing costs may apply.

- It might lower your home’s value if you use the money poorly.

Home Equity Loan vs. Home Equity Line of Credit (HELOC)

A home equity line of credit (HELOC) is different from a home equity loan. HELOC works like a credit card, letting you borrow money as needed up to a limit. You pay interest only on what you use, but rates can be variable.

Home equity loans give you a fixed amount with fixed payments. Choose what fits your needs and budget.

How to Qualify for a Home Equity Loan?

To qualify, lenders check:

- Your credit score and credit history.

- Your income and debt-to-income ratio.

- Your home’s current value.

- The amount of equity you have.

Better credit and more equity increase your chances of approval and better rates.

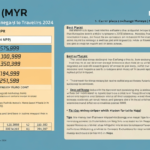

How Much Can You Borrow with a Home Equity Loan?

You can usually borrow up to 80-85% of your home’s equity. For example:

- Home value: $350,000

- Mortgage owed: $250,000

- Equity: $100,000

- Borrow up to 85% of equity = $85,000

Remember, don’t borrow more than you can comfortably repay.

When to Use a Home Equity Loan?

Here are some smart reasons to consider a home equity loan:

- Paying for home improvements.

- Consolidating high-interest debts.

- Covering education costs.

- Financing a major purchase.

- Emergency expenses.

Avoid using it for everyday expenses or things that don’t add value to your life.

Tips for Getting the Best Home Equity Loan

- Compare offers from different lenders.

- Check interest rates and fees carefully.

- Understand the loan terms fully.

- Don’t borrow more than necessary.

- Plan your repayment carefully.

How to Apply for a Home Equity Loan?

Applying is simple:

- Gather documents like proof of income, mortgage statements, and home value info.

- Shop around for the best lender.

- Submit your application.

- Get an appraisal of your home.

- If approved, sign the loan agreement and get your money.

Common Mistakes to Avoid with Home Equity Loans

- Borrowing more than you can pay.

- Using the loan for non-essential spending.

- Ignoring fees and terms.

- Not having a repayment plan.

Being smart and cautious keeps your home and finances safe.

Personal Story: How a Home Equity Loan Helped Me

When I needed to fix my roof, I didn’t want to pay high-interest credit card bills. I took a home equity loan with a low fixed rate. The payments were affordable, and my house value increased after the repair. It was a smart way to manage my money and keep my home safe.

Frequently Asked Questions (FAQs)

1. Is a home equity loan the same as a mortgage?

No, a home equity loan is a second loan using your house’s value, separate from your original mortgage.

2. Can I lose my home with a home equity loan?

Yes, if you don’t repay, the lender can take your home since it’s used as collateral.

3. What is a good credit score for a home equity loan?

Usually, a score of 620 or higher is needed, but better scores get better rates.

4. How long does it take to get a home equity loan?

It can take a few weeks due to the appraisal and approval process.

5. Are home equity loan interest rates fixed?

Yes, most home equity loans have fixed rates, meaning your payments stay the same.

6. Can I use a home equity loan to pay off credit cards?

Yes, many people use it to consolidate debt at a lower interest rate.

Conclusion

A home equity loan can be a smart way to borrow money using the value of your home. It helps pay for big expenses with lower interest rates and fixed payments. But, it’s important to borrow wisely and understand all the risks. Always compare your options and choose what works best for your budget.

If you think a home equity loan might be right for you, start by checking your home’s value and talking to trusted lenders. Your home is a big asset—use it carefully and make your money work for you!